Thermal coal prices: the India factor

Published by Jonathan Rowland,

Editor

World Coal,

Matthew Boyle, CRU.

Supply and demand side developments in India will be an important determinant of future market dynamics and prices for thermal coal according to analysis in CRU's new Thermal Coal Market Outlook service.

The possible volatility in import requirements is substantial, given considerable uncertainty over both domestic supply and demand. Potential volatility in imports or range of outcomes is exacerbated by the fact that India is largely self-sufficient in thermal coal, and its imports account for only ~20% of its demand.

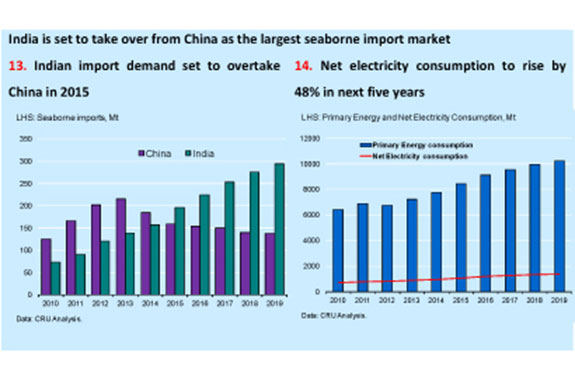

India's domestic demand in 2014 equalled around 80% of the global seaborne market, which means that small changes in supply and demand can have a relatively large impact on total import requirements. Even if domestic coal production was to increase, there would still be issues getting the coal to market due to logistical bottlenecks. CRU has undertaken scenario analysis of potential forecast changes to India's imports, and suggests given the wide range of outcomes, its impact will be felt by the seaborne market.

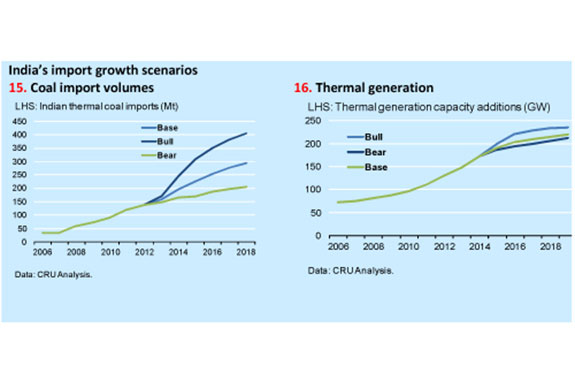

- Under CRU's base case scenario, Indian domestic production is expected to grow at a CAGR of 4.8%, while Indian coal-fired capacity growth is expected to grow at a CAGR of 5.1%. Power capacity utilisation rates in India, which have fallen in recent years, are expected to gradually recover, yet remain below historic levels. Under this scenario, Indian demand is expected to grow at a CAGR of 6.8%, but critically, import requirements are expected to grow at a CAGR of 12.5%, highlighting import sensitivity in such a large market.

- Under a bull case for Indian imports, domestic Indian production will grow at a CAGR of 3%, more in line with historic performance, and consumption to grow in line with current coal-fired construction projects and plans. Under such as scenario, we estimate that total Indian demand would grow at a CAGR of 9% (i.e. only 2.2% higher than in the base case), but import requirements would increase at a staggering 18.5% CAGR.

- Under a bear case scenario for imports, domestic Indian output growth is set closer to current production targets at a CAGR of 7%, whereas consumption growth is limited to the most advanced and likely Indian coal-fired construction projects coming on stream. Under such scenario, we estimate that total demand would grow at a 5.1% CAGR (i.e. only 2.5% lower than in the base case), and import requirements to increase at a very modest 5.4%, adding only 8-10 Mt to total imports/y.

India will be instrumental in determining how much seaborne material will be available for delivery to China, which acts as the clearing market, and remains a key pricing driver. The difference in Indian import volumes between the base case and the two scenarios is 90-110 Mt on either side, equivalent in size to the entire South Korean market.

India's coal industry, in many ways, is at a cross-roads. After a number of years of less than spectacular domestic production growth failing to keep up with power consumption growth, and in turn, a significant increase in and reliance on imported thermal coal, the new Modi government has stepped up plans to increase domestic coal production and power generation. The reallocation of domestic coal blocks, interaction with labour unions and the approval of forest clearances are all signs the government is willing to push ahead with domestic output growth. Whilst the plans are aggressive and needed to reverse an almost paralysed domestic coal industry, we maintain the view that unless there are seismic changes in Indian policy and red and green tape, we are not as optimistic as the government's domestic coal production targets. We estimate Indian coal output to be 599.0 Mt in 2014 with CAGR of 4.8% between 2013 and 2019.

The imbalance between thermal coal production and thermal coal demand growth looks set to continue over the forecast period, requiring an additional 136 Mt of imports by 2019. The majority of this import growth is expected to materialise over the next three years as significant coal-fired capacity comes on stream, and CRU expects India to replace China as the world's largest import market by 2015-2016.

For more information on CRU’s suite of coal strategic forecasting and cost analysis services, or to speak to CRU’s analysts about our market views, please contact Sameer Virani.

Written by Matthew Boyle. Edited by Jonathan Rowland.

About the author: Matthew Boyle is Principal Consultant at CRU.

Read the article online at: https://www.worldcoal.com/special-reports/18022015/thermal-coal-price-outlook-1915/

You might also like

Recycling through neutralisation: How mines can reduce freshwater dependency and costs

Jane Marsh, Editor-In-Chief at Environment.co, details how water recycling through neutralisation helps coal mines reduce freshwater consumption and improve long-term operational resilience through efficient water treatment and reuse.